What is non-financial disclosure?

Non-financial disclosure is the process of reporting on non-financial aspects of a company’s performance, including environmental, social, and governance (ESG) matters. These reports communicate how a company addresses ESG risks and how future financial results can be affected by those risks.

In essence, this process provides stakeholders with a wide picture of the company, their measures, and its goals. It enables them to evaluate the company’s non-financial performance. In other words, ESG reporting shows stakeholders whether the company is solely driven by profit, or whether and how it is committed to positively contributing to society.

In this article, we will take a look at why non-financial disclosure matters for:

- Investors;

- Consumers;

- Regulatory compliance.

On top of that, we will deep-dive into the new Corporate Sustainability Reporting Directive (CSRD) and how it differs from its predecessor, the Non-Financial Reporting Directive.

Why does non-financial disclosure matter?

For investors

Non-financial or ESG reporting has become increasingly popular. Especially among investors, who use the data to incorporate long-term sustainability risks into their decision making. Through reporting on ESG performance, companies show investors that they can mitigate risks and generate sustainable financial returns. If you take the UK as an example, around £6,5bn (€7.6bn) assets under management are ESG-related investments.

Investors also need to know this information to meet their own requirements under the EU Sustainable Finance Disclosure Regulation (SFDR). With sustainability being on the radar like this, a company risks losing investors if it fails to take it into account.

For consumers

Both investors and companies are also driven by changing consumer behaviour. It seems that millennials and Gen Z are putting more and more importance on ESG matters. These issues are at the heart of their consumption habits.

According to a recent study from the Bank of America, 80% of Gen Z consumers factor ESG into investing decisions. IBM has also concluded that 60% of consumers would change their purchasing habits to reduce negative impact. And a study from McKinsey highlighted that 67% and 63% of consumers consider the use of sustainable materials and the brand’s promotion of sustainability, respectively, to be an important purchasing factor.

Regulatory compliance

Regulators and policymakers are also becoming more aware of the role that companies play in solving our social and environmental problems. If companies don’t change their behaviour, we will not be able to eradicate issues such as forced labour or pollution. Non-financial disclosure is a useful tool to monitor if and how companies comply with laws and regulations.

Stakeholders are shifting their attention towards ESG. So, it is no surprise that companies must adapt. They need to fulfil the demands and expectations by reporting on their non-financial matters.

Despite the pressure, many companies lacked behind on their reporting. Those that did report often didn’t deliver the information stakeholders were actually interested in.

That is where the European Commission’s Directive on Non-Financial Reporting comes in.

What are the benefits of non-financial reporting for companies?

- Overall value creation

- Positive influence on stock price performance

- Avoidance of negative impacts

- Increase in investments

- Better reputation (‘corporate branding’)

- More sustainable business model

- Market competitiveness

- Greater talent acquisition and job creation (increasing number of people want to work for responsible companies)

- Better relationship and communication with stakeholders

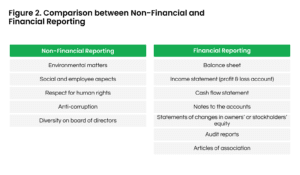

What is the difference between non-financial and financial reporting?

Figure2: The difference between non-financial and financial reporting

The Non-Financial Reporting Directive Explained

In 2014, the European Commission adopted the Directive on Non-Financial Reporting (NFRD), with an aim to strengthen accountability and to help stakeholders to monitor and evaluate the ESG performance of target companies. In essence, the Directive requires certain large companies to disclose information regarding their operation and management of ESG challenges.

The EU Member States have the freedom to implement the Directive as best suits their national interest. They only need to meet the minimum requirements. They are free to further specify what counts as non-financial matters or choose the level of regulatory intervention.

The level of implementation also depends on any existing laws in the given member state. Despite the discretion, almost half of the Member States took the easier way out and simply inserted the exact text of the Directive into their national legislations.

The Corporate Sustainability Reporting Directive Explained

The new Corporate Sustainability Reporting Directive (CSRD) has been adopted on the 21st of April 2021. The current NFRD raised concerns about:

- Quality;

- Consistency;

- A lack of information on sustainability-related risks.

The CSRD wants to provide more verifiable, accessible and coherent non-financial data. On top of that, it aims to ensure alignment between non-financial and financial standards. It is developed in accordance with the European Green Deal and the UN Sustainable Development Goals.

A new reporting standard should enable stakeholders to better compare various reports and ensure the trustworthiness of the disclosed information. It also seeks to ultimately minimize the cost of reporting for companies in the long term.

There is a growing demand from stakeholders to disclose non-financial performance. The Commission argues that most companies would face an increase in costs if they continue to report under the current frameworks. This is largely due to the existence of several overlapping standards requesting inconsistent information and requiring multiple reporting.

The CSRD might imply additional costs in the short term, it is believed to be less costly over time. It is believed that the new Directive will also create greater public accountability.

In line with the European Green Deal, the CSRD will also aim to reduce any risks to the economy and improve the allocation of financial capital to companies that address sustainability issues. As such, the CSRD is closely linked to two other key regulations: EU Taxonomy and Sustainable Finance Disclosure Regulation.

The CSRD is currently being rolled out. It is estimated that companies will have to start reporting under it from 2024 (to report on the financial year 2023).

What must be disclosed under the NFRD?

Under the NFRD, companies must provide information on the following topics:

- Environmental matters

- Social matters and treatment of employees

- Respect for human rights

- Anti-corruption and bribery

- Diversity on company boards

In general, the disclosure must include:

- A description of the company’s business model

- Description and outcome of policies

- Related risks to the company’s operations

- Non-financial KPIs (related to the environment, social and employee issues, human rights and corruption and bribery)

The Directive requires the above to be disclosed in annual reports, sustainability reports or other integrated reports. The company is required to publicly explain if it fails to report on any of these. Requiring them to report not only on what they have and do but also on what they lack. This holistic approach creates greater accountability as no company wants negative publicity.

The NFRD also applies double materiality, meaning that companies are not only required to disclose how sustainability issues affect them (financial materiality) but also the impact the company has on the society and environment.

What must be disclosed under the CSRD?

The new CSRD will require companies to assess how their strategy and business model aligns with and impacts sustainability matters. More specifically, the reporting will have to cover:

- Overall company strategy including double materiality and strategy alignment with the transition to a greener economy

- Stakeholder engagement

- Future sustainability ambitions and targets

- Past sustainability performance

- Policies and processes across the entire value chain

- Risk management

- Reporting process

Companies will be required to include sustainability reporting in their management reports in a digital and machine-readable format.

As such, the CSRD aims to get a more holistic view of companies’ sustainability efforts compared to the NFRD. While the NFRD has more of a retrospective view and focuses on five specific topics, the CSRD looks at both past performance and future strategy related to broader sustainability initiatives and how risk is mitigated. This should result in reporting that showcases the overall sustainability performance.

Who must report in accordance with the NFRD?

The Directive applies to large public companies, with more than 500 employees, and mainly affects listed companies, banks, and insurance companies. The Directive also applies to all operations within the EU, meaning that any non-EU company will have to adhere to this Directive with regards to their EU operations. The EU estimates that the Directive applies to around 11 700 companies across the EU.

Who must report under the new CSRD?

Under the new CSRD, the scope will be extended to include all large companies, all companies listed on the European stock exchange, and publicly listed small and medium sized companies. Additionally, subsidiaries of global non-EU firms and companies that are not incorporated in the EU but have securities on EU-regulated markets, will also have to comply to the reporting.

The definition of large companies will also change under the CSRD. Companies will fall under the ‘large company’ definition if they meet 2 of these 3 criteria: €40 million in net turnover; €20 million on the balance sheet, and 250 or more employees.

How to report using the NFRD?

The Commission has provided a set of guidelines to assist companies on how to disclose this information. However, these are not mandatory to follow. Instead, companies can decide to use any other international, European, or national guidelines to disclose this information.

The GRI standards have so far been the most used framework, followed by the ISO 26000 Guidance on Social Responsibility, Social Accountability 8000 and the OECD Guidelines for Multinational Enterprise. When reporting, the company simply states which framework has been used.

Due to the lack of alignment, the Commission has published a New Consultation Document on the Update of the Non-Binding Guidelines on Non-Financial Reporting. The updated guidelines seek to further align with the TCFD.

How to report using the CSRD?

Companies will have to report according to mandatory EU Sustainability Reporting Standards that will be published by the end of 2022. The standards will take into account global initiatives including GRI and SASB.

CSRD will also require companies to audit the reported information. Previously, this was not mandatory (although some countries made it a national requirement). Non-compliance will be penalized, based on national laws.

In addition, the reporting under CSRD aims to fully align with the Sustainable Financial Disclosure Regulation (SFDR) and EU Taxonomy.

The SFDR came into force in early 2021 and is part of the EU’s Sustainable Finance Action Plan. It introduces requirements for financial market participants (asset managers, financial advisers and insurance providers) for disclosing sustainability-related information. Such standardized disclosure should enable investors to make more informed and sustainable investment decisions.

The EU Taxonomy is a classification system used to identify environmentally sustainable investments, enabling investors to make greener choices. Companies in scope for NFRD and financial participants in scope for SFRD, have to report on their alignment with the Taxonomy.

What’s next?

EU regulations and legislations regarding sustainability keep evolving so we should expect further requirements and clarifications. While it can be a little difficult to wrap our heads around all the initiatives and links between them, it is comforting to know that the EU is clearly putting effort into ensuring that the European future is greener and more sustainable.

For more information, please refer to the European Commission’s website.

Other reporting regulations/ legislations/ recommendations

There are already many other regulations concerning non-financial disclosure, including

- UK’s Modern Slavery Act;

- French Law on the duty of care of parent companies and ordering companies;

- Italian Regulations on disclosure, advertising and implementation of insurance products;

- the EU’s Anti-Money Laundering Directive.

And it is estimated that the number will continue to grow.

Apart from regulations, there are also several other initiatives that promote the importance of non-financial reporting. The Task Force on Climate-Related Financial Disclosures (TCFD), World Economic Forum, The World Federation of Exchanges and the World Council for Sustainable Development, just to name a few, all publish their own recommendation on how non-financial disclosure should be managed and disclosed.